Converting currencies with Interactive Brokers can be confusing at first, so, as a follow-up to my post on paying as little commission as possible when converting US and Canadian dollars, here’s a quick tutorial on how to do that.

1) Linking Accounts

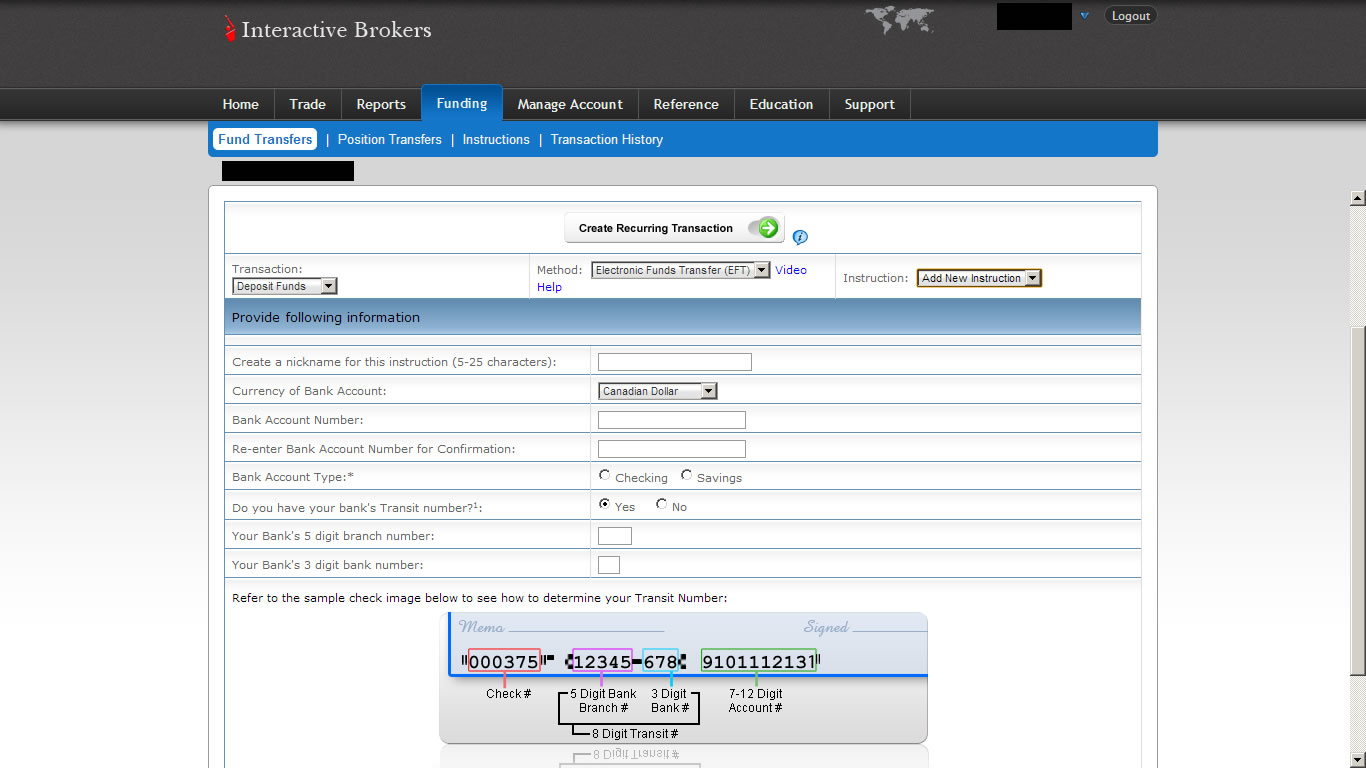

If you’d like to fund your account via ETF, you’ll need to configure your bank accounts in your Interactive Brokers (IB) account. For that, you need to add what they call an “Instruction”. They’ll then make a small deposit in your bank account, you’ll confirm the amount and you’ll then be able to use the instruction to transfer funds in and out of your IB account, subject to their hold policy.

Canadians can link both CAD and USD-denominated bank accounts held at Canadian banks to their IB account.

You can add Fund Transfer Instructions in the Account Management area of the IB website:

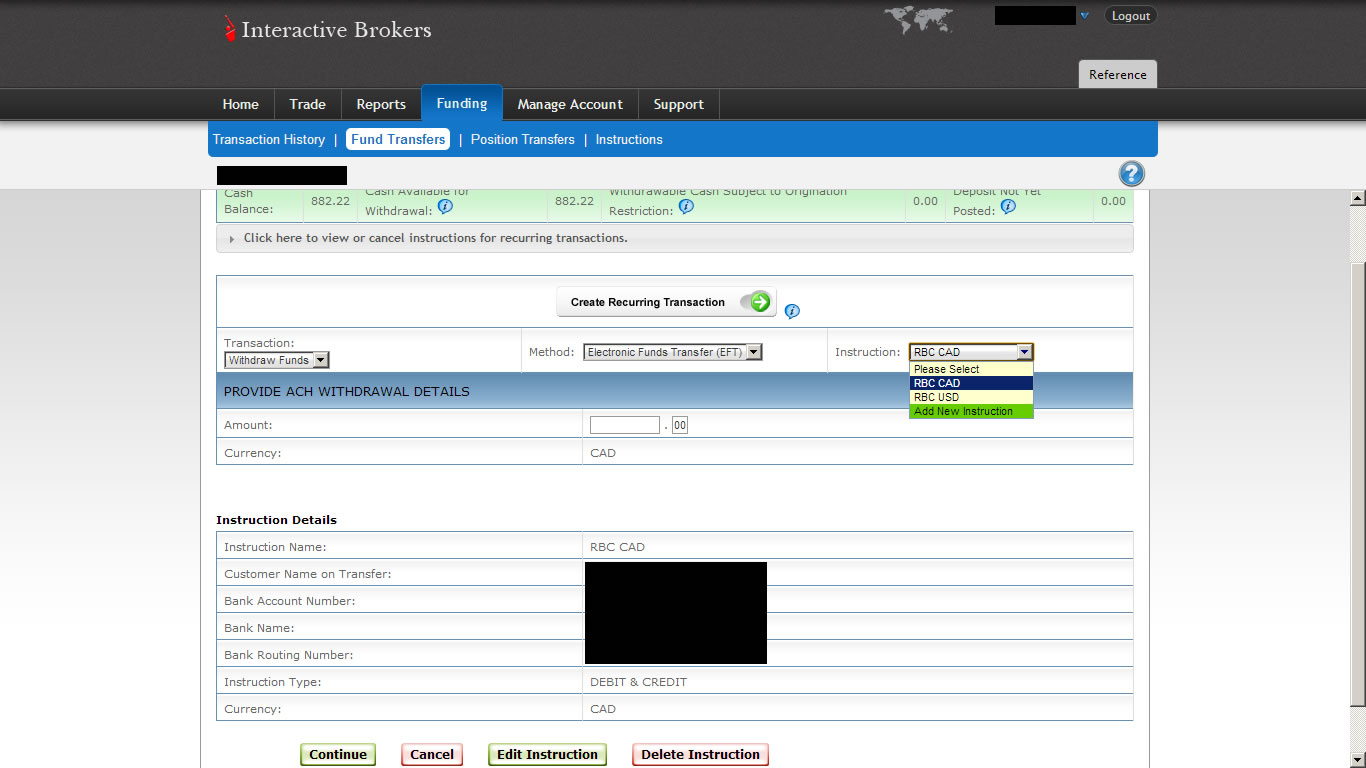

Once you’ve validated the instruction by entering the small deposit amount that you’ve received from IB to verify your bank account, you can deposit/withdraw funds by creating a Fund Transfer Instruction, also in your Account Management area:

More information: Funding your account | Withdrawals

2) Converting Currencies

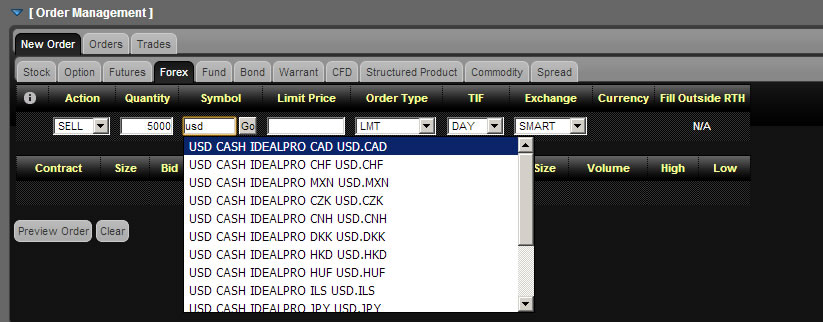

2.1) Log in to the Web Trader platform

2.2) In the order management section, choose Forex, and select Buy if you want to buy USD, and sell if you want to sell USD. Enter the amount of USD you want to sell for a SELL order, or the amount of CAD you want to convert to USD for a BUY order.

2.3) In the symbol field, type “USD” and then click the “Go” button. You should be able to choose the USD.CAD currency pair in the drop-down:

2.4) Change the order terms (order type, limit price, etc.) if you’d like.

2.5) Click “Preview Order” and make sure the information is accurate and that you’ve entered the correct amount in the source/destination currency (so you don’t end up selling the equivalent of 5000 CAD instead of 5000 USD, for example):

2.6) Click “Submit Order” and wait for your order to be filled (almost instantaneous for market orders during market hours, while limit orders may or may not be executed depending on your limit price).

That’s it! The interface may look scary at first, but I find it’s well worth the savings if you’re converting tens of thousands of dollars per year through Interactive Brokers.

3) What to do afterwards?

Depending on how you funded your account, there may be a rather long hold period for your funds (currently 3 business days for wire transfers and 60 business days for EFTs). You may leave the funds in your cash balance while waiting for the hold to expire, or you can use them to buy stocks/ETFs if you prefer. I tend to buy short-term bond ETFs like XSB and sell them after the hold period ends, but that’s a matter of personal preference.

***

I hope this information was helpful. Don’t hesitate to post in the comments if you appreciated it (it’s always nice to see that people liked a blog post) or if you have any question.

")